The break-even point is the point at which total cost and total revenue are equal, meaning there is no loss or gain for your small business. In other words, you’ve reached the level of production at which the costs of production equals the revenues for a product.

For any new business, this is an important calculation in your business plan. Potential investors in a business not only want to know the return to expect on their investments, but also the point when they will realize this return. This is because some companies may take years before turning a profit, often losing money in the first few months or years before breaking even. For this reason, break-even point is an important part of any business plan presented to a potential investor.

For existing businesses, this can be a useful tool not only in analyzing costs and evaluating profits they’ll earn at different sales volumes, but also to prove their potential turnaround after disaster scenarios.

Benefits of a break-even analysis:

✔ Price Smarter

✔ Catch Missing Expenses

✔ Set Revenue Targets

✔ Make Smarter Decisions

✔ Limit Financial Strain

✔ Fund Your Business

Tips and tricks

Use the break-even formula

This break-even analysis is based on the foundation of a single product or service.

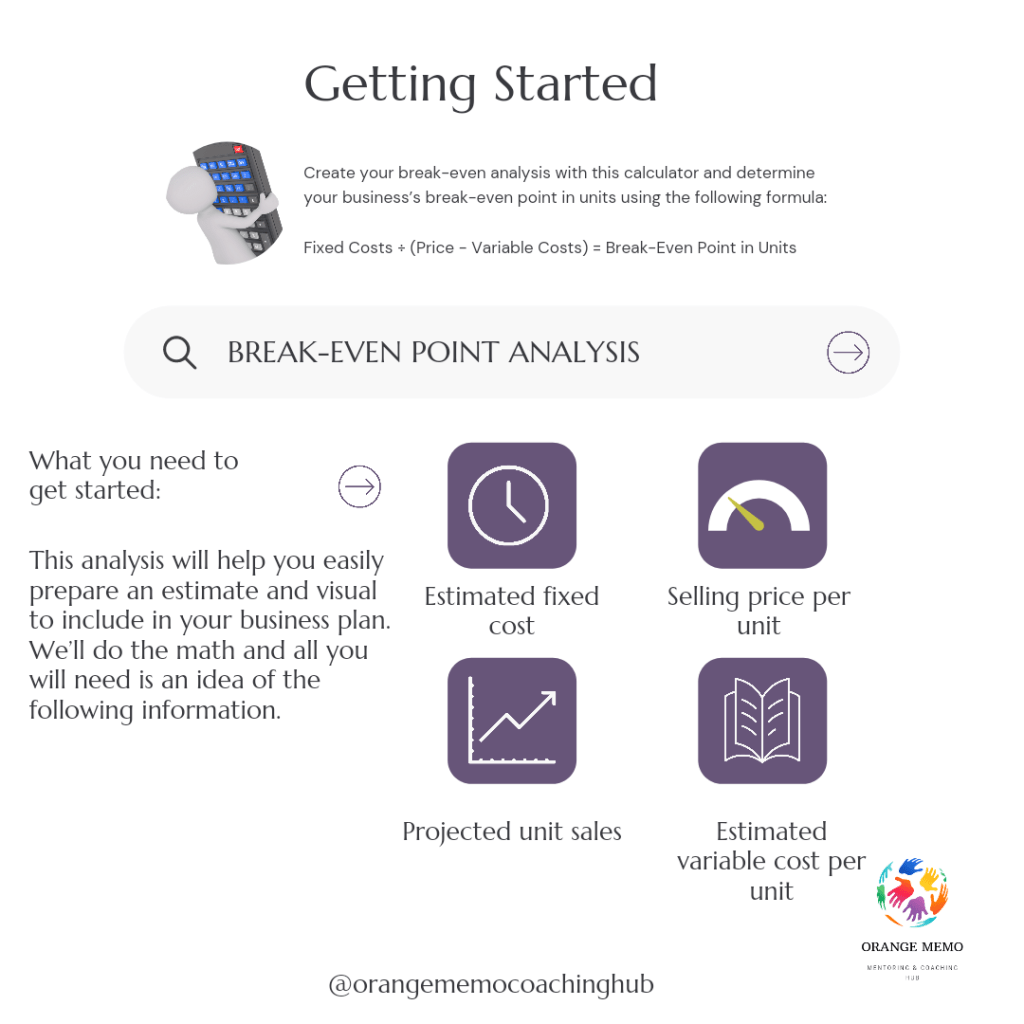

To calculate the break-even point in units we use the formula:

Break-even point (units) = fixed costs ÷ (sales price per unit – variable cost per unit)

Or in sales rands (dollars) using the formula:

Break-even point (sales dollars) = fixed costs ÷ contribution margin

Contribution Margin is the difference between the price of a product and what it costs to make that product.

The calculation is as follows:

Contribution margin = (sale price per unit – variable cost per unit) ÷ sale price per unit

Calculate multiple products or services

The total fixed costs, variable costs, unit or service sales are calculated on a monthly basis in this calculator. Meaning that adding the total for all products and services monthly should account for all products and services. You may also want to do the calculation individually for each product or service if the products or service sales vary per month.

Remember the break-even point is used as an estimate for lender viability and your business plan. It is not intended to 100% accurately determine your accounting or financing since those calculations can only be done after all costs and production have occurred. It’s also a good idea to throw a little extra, say 10%, into your break-even analysis to cover miscellaneous expenses that you can’t predict.

Learn about fixed costs

Fixed costs are costs incurred during a specific period of time that do not change with the increase or decrease in production or services. Once established, fixed costs do not change over the life of an agreement or cost schedule. For this calculator we are calculating the fixed costs on a monthly basis.

If you have fixed costs that do not incur monthly you should still include them, but calculate the monthly amount that goes towards that expense. For example if something is paid for on a quarterly basis, but does not change with production you would divide that cost by four in order to estimate the monthly amount of that cost. In the break-even analysis we will help you break down the potential fixed costs related to your business.

Examples of fixed costs include:

• Rental lease payments

• Salaries

• Property taxes

• Insurance

• Interest

Learn about semi-variable costs

Sometimes determining whether a cost is fixed or variable is more complicated.

There is also a category of costs that falls in between, known as semi-variable costs (also known as semi-fixed costs or mixed costs). These are costs composed of a mixture of both fixed and variable components. Costs are fixed for a set level of production or consumption and become variable after this production level is exceeded. If no production occurs, a fixed cost is often still incurred.

The best way to include these costs is to separate out the part that is variable from the part that is fixed. These may include minimum payments or fees for services and products. For the break-even analysis to be as accurate as possible it is important to separate any semi-variable costs into their fixed and variable parts if possible.

Examples of semi-variable costs include:

• Monthly telephone services

• Repairs

• Indirect materials

• Indirect labor

• Fuel

• Power

NOTE!

Do ask for help. Sometimes it is difficult to estimate and project data. Feel free to email me at gugu@orangememo.co.za and I will gladly help you (in the subject line please put “Break-Even Analysis: need help with the “estimates and projections”).

One thought on “Break-Even Point”